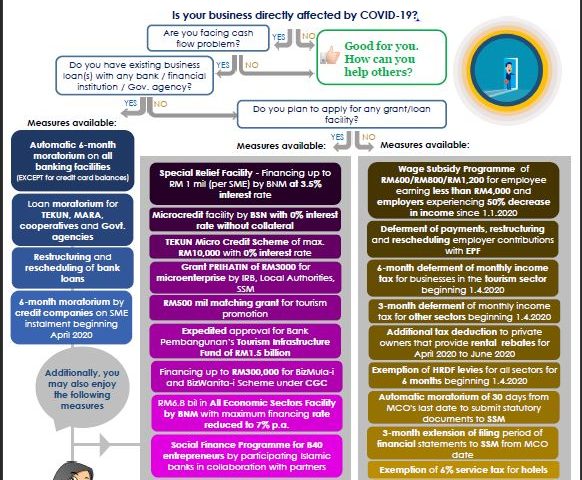

We are now living in unprecedented times of a global pandemic due to COVID-19. During this ongoing crisis, the Government recognizes the challenges faced by individuals, businesses and the economy at large

Program subsidi upah adalah bantuan kewangan yang dibayar kepada semua perusahaan yang terkesan dari segi ekonomi akibat Covid-19 bagi tujuan dapat meneruskan operasi syarikat serta mengelakkan pekerja hilang pekerjaan dan punca pendapatan

KWSP LANCAR e-CAP BAGI MENYOKONG PKS YANG TERJEJAS AKIBAT COVID-19

KUALA LUMPUR, 23 April 2020: Kumpulan Wang Simpanan Pekerja (KWSP) melancarkan Program Bantuan Majikan COVID-19 (e-CAP) untuk memberi sokongan kepada perusahaan kecil dan sederhana (PKS) yang terjejas akibat pandemik global COVID-19.

9 Persoalan Dan Masalah Yang Kerap Dihadapi dalam Permohonan Geran Prihatin Mikro

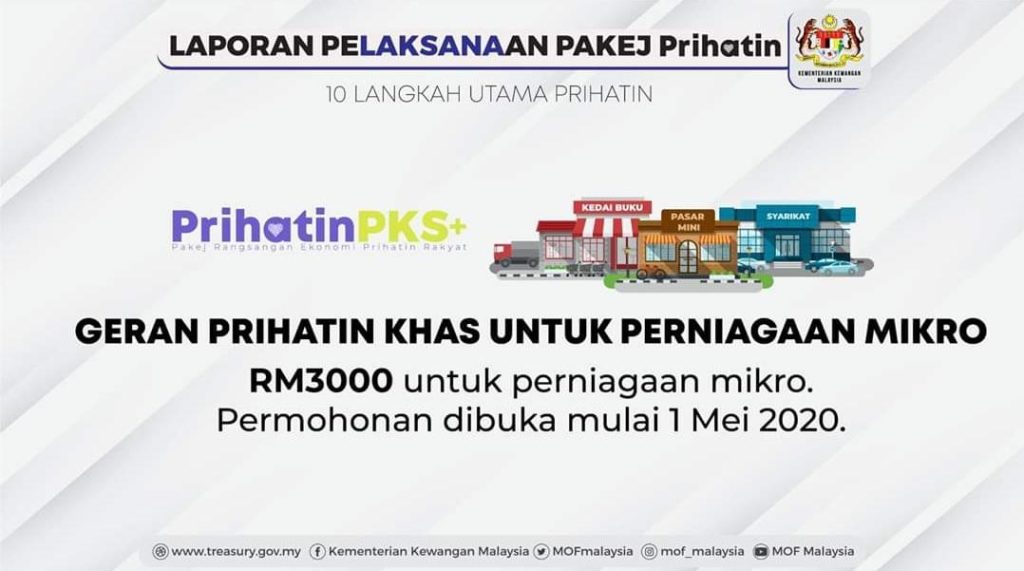

Geran Prihatin khas untuk mikro iaitu peniaga kecil dan sederhana. Maksudnya peniaga yang mempunyai ✅Pendapatan tahunan dibawah RM300 ribu ✅Memiliki 5 orang pekerja dan kebawah, tidak termasuk pemilik. ✅Mempunyai SSM atau daftar LHDN atau pihak berkuasa tempatan sebelum 31Dec2019.

Wabak Covid-19 telah menjejaskan aktiviti ekonomi negara Malaysia dan telah menyebabkan Perusahaan Kecil dan Sederhana telah mengalami kerugian kerana aktiviti ekonomi telah terhenti disebabkan wabak ini.

Skim Pembiayaan Pemulihan Perniagaan Sektor Mikro TEKUN Nasional (CBRM)

Skim Pembiayaan Pemulihan Perniagaan Sektor Mikro TEKUN Nasional (CBRM) ialah skim pembiayaan mikro bagi usahawan yang terjejas kesan daripada wabak COVID-19 untuk memulih dan memulakan semula perniagaan sedia ada.

In view of the extension of the Movement Control Order announced by our Prime Minister on 25 March 2020, the submission and payment deadlines for any returns or payments to the Royal Malaysian Customs Department have been further extended to 30 April 2020.

SOALAN – SOALAN LAZIM Program Subsidi Upah (Wage Subsidy)

Apakah itu Wage Subsidy? i. Wage Subsidy merupakan langkah penambahbaikan kepada usaha Kerajaan untuk majikan mengekalkan pekerja

ii. Wage Subsidy adalah subsidi upah sebanyak RM600 sebulan kepada majikan bagi setiap pekerja yang bergaji RM4,000 dan ke bawah (terhad kepada 100 orang) untuk tempoh 3 bulan.

Apakah objektif Wage Subsidy? i. Membantu majikan yang terkesan dari segi ekonomi akibat COVID-19 supaya dapat meneruskan operasi syarikat serta mengekalkan pekerja mereka.

Q1. What are the criteria to receive Wage Subsidy? a) Employers and Employees have to be registered and contributed Employment Insurance System (EIS); b) Employers have to make declaration that the company suffered declining revenue more than 50%,by comparing with the total sales in January 2020 with the following months; c) Employees with the wages of RM4,000-00 and below, subject to 100 pax; d) Employers have to ensure they will not (i) dismiss the Employees, (ii) instruct the Employees to take unpaid leave; and (iii) deduct salary for 6 months

Skim Peka PKS peruntuk RM30 juta bantu IKS dan PKS

GEORGE TOWN – Kerajaan Negeri hari ini mengumumkan peruntukan RM30 juta melalui Skim Pinjaman Kelangsungan Perniagaan Pulau Pinang atau secara ringkasnya, Skim Peka PKS khas kepada usahawan-usahawan Industri Kecil dan Sederhana (IKS) dan Perusahaan Kecil dan Sederhana (PKS) di negeri ini

Malaysia’s Service Tax is a form of indirect single stage tax imposed on any provision of taxable services made in the course or furtherance of any business by a taxable person in Malaysia.

THE Inland Revenue Board Malaysia (LHDN) has issued a new Tax Investigation Framework 2020 to replace the Tax Investigation Framework issued on May 15, 2018.

In every business, whether it is small or big, it requires constant attention so that the business can run smoothly. Among all these elements, accounting and bookkeeping method is an important one.

Malaysia Immigration Visa Application for foreigners: Expatriate DP10 Work Visa for you and family Our service includes the application of dependent visa and ID card for the expatriate and his family

Limited Liability Partnership (LLP) is an alternative business vehicle regulated under the Limited Liability Partnerships Act 2012 which combines the characteristics of a company and a conventional partnership.

“Digital services” is defined under the Amendment Act to mean any service that is delivered or subscribed over the internet or other electronic network and which cannot be obtained without the use of information technology (IT) and where the delivery of the service is essentially automated.

Trademark means any sign capable of being represented graphically which is capable of distinguishing goods or services of one undertaking from those of other undertakings. ————————-

Malaysia is a prime business destination envied by thousands of investors keen on starting ventures abroad. In Asia the most stable political and economic systems.

Monthly Tax Deduction (MTD or PCB, Potongan Cukai Bulanan) was introduced in January 1995, is a system of tax recovery where employers make deductions from their employees’ remuneration every month in accordance with the PCB deduction schedule.

Why should I increase my company’s paid-up capital? Normally, there are three (3) reasons where the company may find itself in the situation that it needs to increase its paid-up capital:

Extensible Business Reporting Language, which is also known as XBRL, is an electronic language designed to enable the automation of business information requirements, i.e. the preparation, sharing and analysis of financial reports, statements, and audit schedules.

A company secretary has heavy responsibilities and great power in intermediating between the governmental departments and the business owners. The following are the duties of company secretary in Business Registration

In Malaysia, ‘Shadow economy’ is estimated to be a fifth of the officially reported RM1.45 trillion gross domestic product (GDP) which is why the government is serious about tackling caused by the ‘shadow economy’.

Starting from July 1, 2019, the Companies Commission of Malaysia (SSM) has implemented the automatic compound rate reducing method as a remedial solution for the compound within a specified period.

As expected by economists, Bank Negara Malaysia’s monetary policy committee has maintained the overnight policy rate (OPR) at 3%, and kept its economic growth forecast for this year at between 4.3% and 4.8%.

How to Start a Small Business in Malaysia As a Foreigner

Starting a small business in Malaysia as a foreigner may be easy, and with the right assistance, it can be set up quickly in no time. Here are the other factors that you will want to consider when it comes to how to start a small business in Malaysia as a foreigner:

How much of paid-up capital should I have for my new company? Any amount from at least RM2 up to the maximum of the authorised capital as stated in the M&A (Memorandum & Articles of Association) of the Company, 100,000 for normal new company.

An annual return is a snapshot of general information about a company’s directors, secretary (where one has been appointed), registered office address, shareholders and share capital.

Registered office within Malaysia Within 14 days after the date of its incorporationor the day it begins its business, whichever theearlier, every company shall have a registeredoffice within Malaysia to which all communicationsand notices may be addressed.

There must be one of the following reasons you may want to convert your business from sole-proprietorship (enterprise) or partnership to Sdn Bhd Company (Private Limited Company):

With more complex developments in company legislation and the creation of business collaborations to result in larger groups of companies, the role of a company secretary has evolved from just a normal employee to one who is far more important in any company.

Shareholders can leave a company at any time for several reasons: it may be to remove shareholder from a company, recoup investment or as a result of death.

Malaysia itself is well located within Asia Pacific and Asean! Malaysia with recent ranking being the top 6thcountry in the world as the most easiest and friendliness

We will provide you with local Nominee Directors who are Malaysia citizen and closely associated with the management team in Bayabumi Accountancy, with guaranteed good services.

Extensible Business Reporting Language, which is also known as XBRL, is an electronic language designed to enable the automation of business information requirements, i.e. the preparation, sharing and analysis of financial reports, statements, and audit schedules.

Accounting is a necessary part of the business process and many business owners and entrepreneurs need the services of a good accounting firm in their fold to use them to their best business advantage.

Planning to start your very own business in Malaysia? Then this how to register a Sdn Bhd company in Malaysia guide is exactly what you are going to need as you get started on incorporating your very first company in Malaysia.

Our Annual Financial Audit approach is based on an understanding of our clients’ business processes, goals, and strategies. This enables us to identify and assess the risks that impact their business and achievement of goals

Every company operating in Malaysia must file tax returns every year. This is for resident companies i.e. those that have their management and control based in Malaysia, and non-resident companies i.e. companies that have more than 50% in foreign shareholding.

If you are a foreigner looking to do business in Malaysia, you have the choice of picking the sole proprietor model of business, partnership or a private limited company.

The first stage would involve deciding on the business entity type you’re going to go with. Each entity has its own compliance requirements, benefits and tax structure.

Malaysia as a new highlight in the economics of the ASEAN is a prospective place to set up a company. A lot of business owners around the world compete to set their camp on it as a company.

Malaysia starts stealing the world’s attention for its business potential. A decade ago, this country was mostly known as one of the most favorite tourist destinations in the ASEAN. .

Social Security Organization (SOCSO), or also known as PERKESO (Pertubuhan Keselamatan Sosial) was established on 1 January 1971, under the Employees’ Social Security Act 1969 as a government department of the Ministry of Labour and Manpower.

Malaysia has always been a country that attracts a lot of interest from investors, whether international or local. Why investors would choose to have their company registration in Malaysia has a lot to do with the following factors:

Anyone who wanted to incorporate a business will need to register their company, which first step is the lodgement of company name search application to SSM Malaysia (Suruhanjaya Syarikat Malaysia). By doing so is to seek for SSM’s approval of using the desired name in your new company.

The SSM (Suruhanjaya Syarikat Malaysia) is that the statutory body fashioned in Malaysiato managecorporations and businesses that are wrongfully registered and operational in Malaysia.

Investing your cash and time within theinstitution of a corporation in Malayamay be aniceplan. Malaya shows a positive growth of social science and a stable spectrum of politics.

Corporate tax, or company tax, may be a levy placed on the profits/revenues of an organization and it varies between countries. even asincome taxes will influence the defrayment behaviour of people, company taxes canhave an effect on the approach that companies do business.

Nobody enjoys paying taxes. however taxes are the law. The terms “tax avoidance” and “tax evasion” are typically used interchangeably, however they’re terribly totally different ideas. Basically, minimisation is legal whereas nonpayment isn’t.

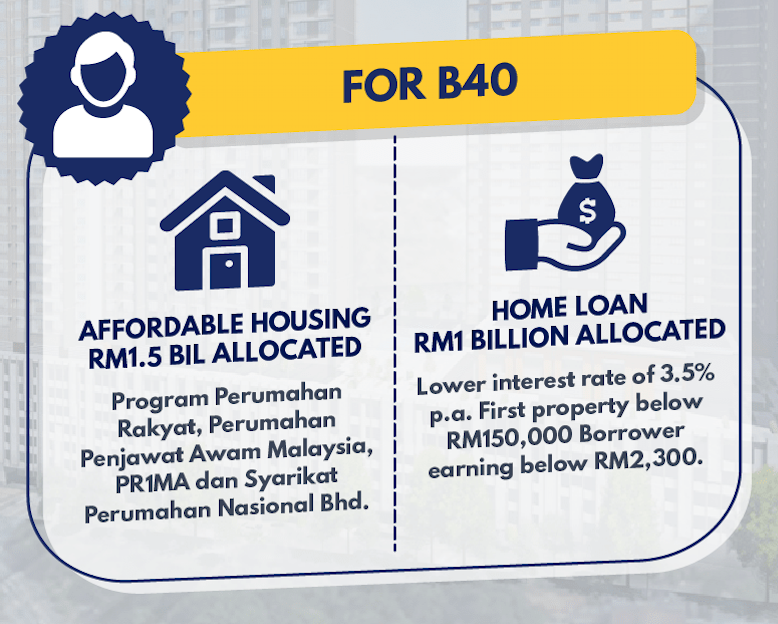

The T20 group is defined with the median household income of at least RM13,148 while the M40 and B40 groups’ median household income have moved their bars up to RM6,275 and RM3,000 respectively,

Beginning 1st January 2019, the Government will offer a free insurance scheme worth RM2 billion to individuals between the ages of 18 to 55 within the 4.1 million B40 households.

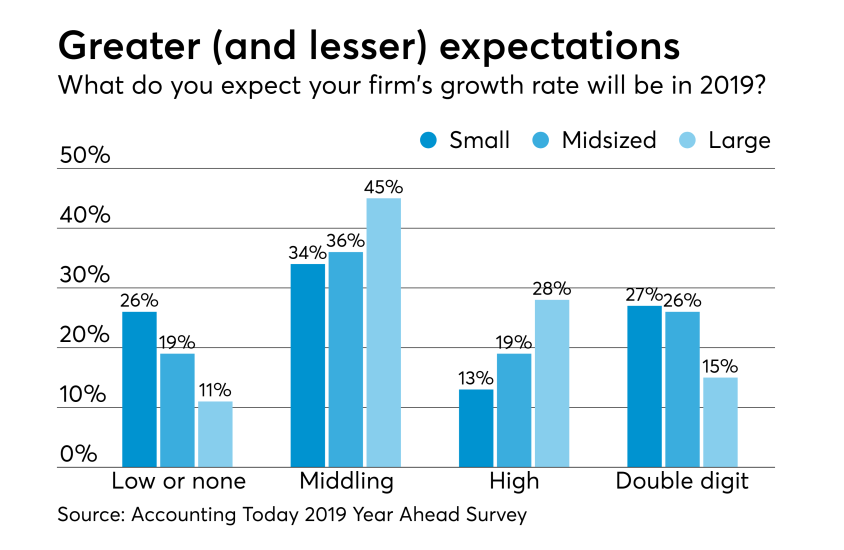

For corporations of all sizes, the foremost common expectation was that they might expertise middling growth in 2019 (from 2-5%), however that masks one thing of a shift from last year, with a lot of corporations probably to report double-digit growth, high growth (from 6-9%) or low or declining growth (1% or less).

1. Enable smart organization for a distributed workforce.

Since accounting info hold on within the cloud is more or accessed anyplace, team members will quickly and simply complete their work no matter their physical location.

Strong businesses have a solid handle on their financial reality, and the cash flow statement is an excellent, if not the best, measure of a company’s ability to generate cash in excess of cash invested.

Malaysia’s ambitions under the Economic Transformation Programme to produce 60,000 accountants by 2020 will require a concerted effort from the accountancy profession

SSM Registered Business Entities to Have New Format for Registration Numbers

Business entities registered in Malaysia will now have a new registration number format when they register with the Companies Commission of Malaysia (SSM). .

15 Items Exempted from Sales and Services Tax (SST)

With the forthcoming Sales and Services Tax (SST) quick approaching, the question on everyone’s mind goes to be that things are visiting be SST exempted items? Are a number of your regular favorites or requirements visiting be suffering from this forthcoming change? Let’s understand. .

per day.

per day.